A financial service matchmaking platform for the underbanked/unbanked people. Users provide their personal data and behavioral preferences hassle-freely through chatbots and mini-apps. The platform uses machine learning algorithms and compliance systems to make precise and real-time financial product recommendations from partnered financial institutions. Whenever a user receives said product/service, the platform shares part of the commission fees with all users.

My Role

I worked as the sole Product Manager, Project Manager, and Quality Assurance Specialist for the aifian app in 2019-2020, partnered with a product director/product designer, a business development manager, and an outsourcing engineering team.

After reshaping the product vision and business model, I was responsible for a 120k-user app revamp project, which went through competitive research, requirements definition, features and processes design, QA testing, public opinion monitoring after launch, and iterations. My responsibilities also include establishing and improving product workflows and systems to ensure that the design and outsourcing engineering team understand the requirements accurately, improving the efficiency of weekly product meeting communication by 50%.

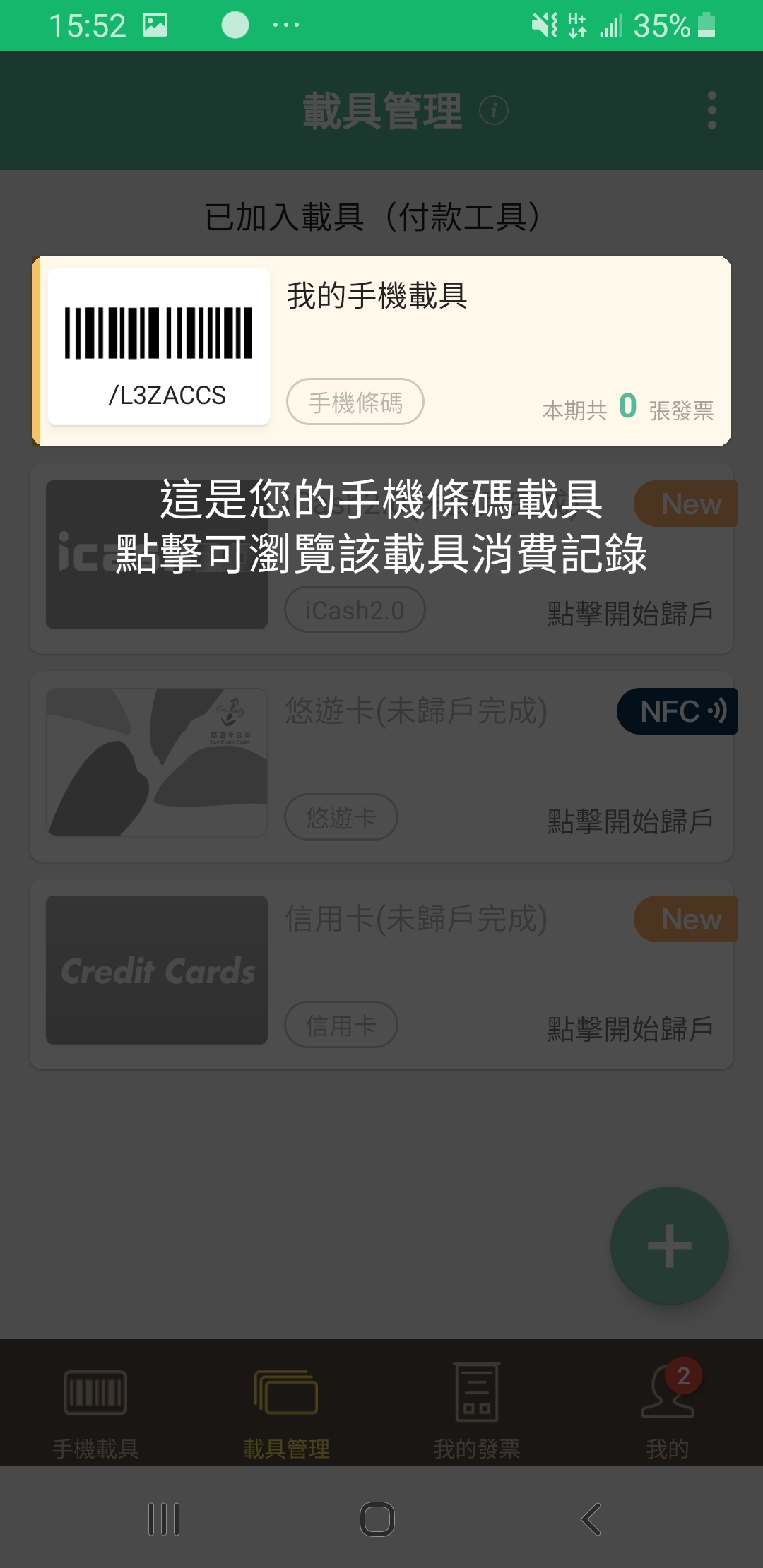

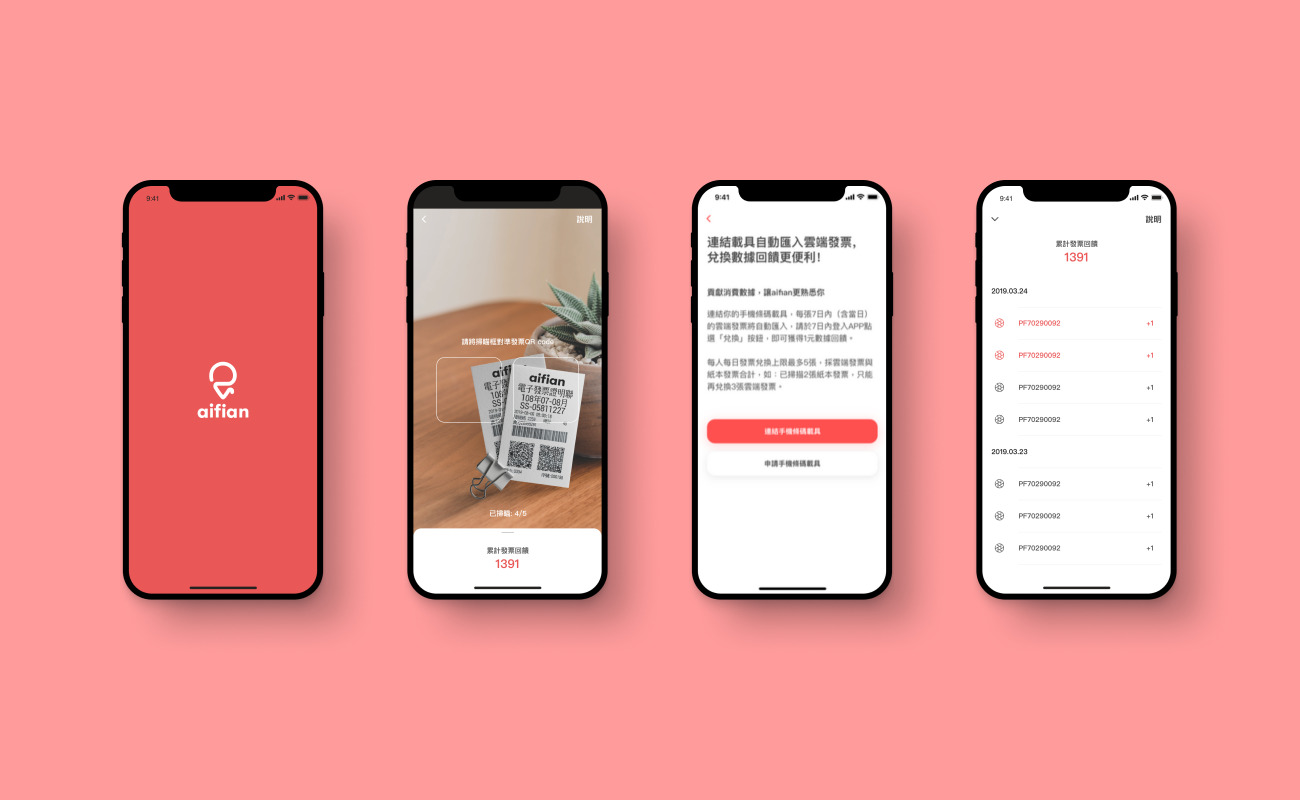

This project improved aifian data collection with user-friendly chatbots and mini-apps that raised 8% retention rate and 6% user authentication rate, and lowered 5% churn rate for the onboarding process. In addition, we successfully onboarded 54% of daily active users to the invoice collector feature illustrated below within a week.

Background

Many young people with a low asset under management (AMU), especially the unbanked/underbanked people, are not the primary audience of traditional financial institutions. They have no or limited access to appropriate and suitable financial products –– either the agreement of the products they obtain is unfavorable to them, or they are simply rejected by those institutions, becoming marginalized for financial services.

aifian is a financial service matchmaking platform. It collects user data such as family, work, and behavioral preferences through chatbots and mini-apps to perform initial screening and compliance checks for financial institutions and make precise and real-time financial product recommendations with AI algorithms.

Through interaction with aifian, users can obtain financial products that best fit their needs in a market with highly similar services and enjoy the benefits of data monetization as cash back. Financial institutions can develop potential customers they could not reach in the past through precise marketing. The platform can optimize the matching system and make more appropriate recommendations to users, improving retention for financial services and creating a win-win and lasting financial loyalty program for three parties.

Problem & Goal

In order to optimize matchmaking algorithms and recommendations, aifian collects various aspects of personal data through identification authentication, payday loan service, etc. In financial respect, most personal data is about “consumption.” The Ministry of Finance in Taiwan also actively promotes paperless “uniform invoices” stored in the cloud for environmental protection. So to achieve the following goals, we decided to develop a feature of “invoice collector” that can link to the cloud database of electronic uniform invoices:

Know our customers better by collecting more user data, such as daily spending records and e-invoice carrier status.

Raise user stickiness and retention by attracting users to open the app on a daily basis, solving the problem of low frequency for financial services.

What is Uniform Invoice?

In Taiwan, receipts with an 8-digit number are called “Uniform Invoice (統一發票).” Every two months, there is a lottery-like drawing by the Ministry of Finance to incentivize consumers to make purchases at sellers legally reporting taxes and thus encourage businesses to keep every above board. Winner can redeem prizes ranging from $200 NTD to $10 million NTD.

Image source: Taipei Expats

Research

In the early stage of this project, we conducted market research to understand how consumers manage their paper and cloud e-invoices. The followings are what we found:

Invoice passbook, invoice carrier setting, and invoice lottery checker are 3 kinds of expected features (the must-have requirements in Kano Analysis) for every invoice management app.

Only few invoice management apps allow users to earn points and exchange merchandise with it, indicating that the demand for invoice data monetization has gradually emerged but has not yet been satisfied.

Here are some main features and screenshots of invoice management apps:

Invoice Scanner

Invoice Passbook

Carrier Management

Invoice Lottery Checker

Merchandise Redemption

aifian users asking for commonly used features on Google play.

Define

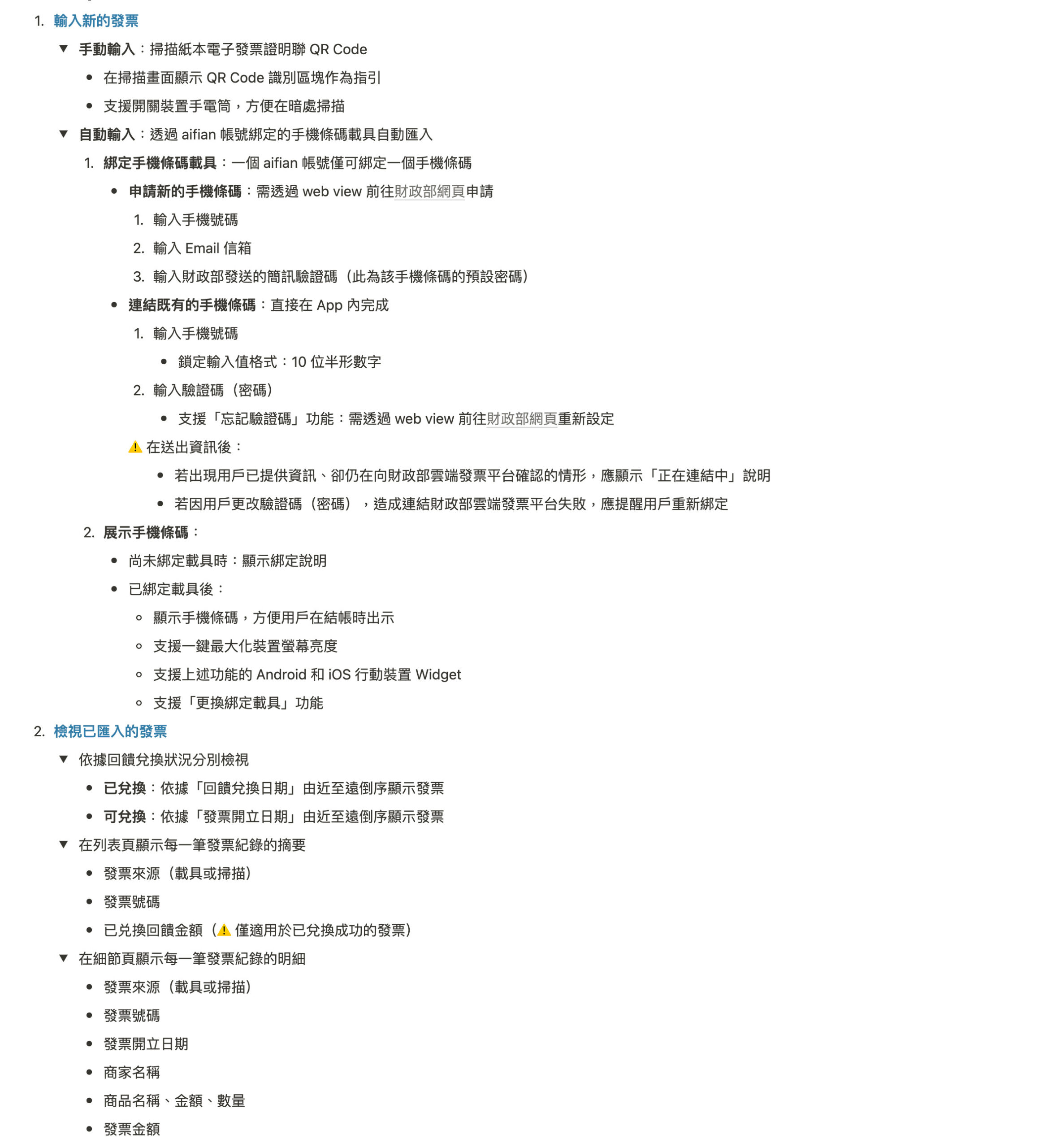

Considering the product positioning of aifian is a matchmaker based on personal data, we focused on invoice data import rather than invoice management and scoped out the feasible MVP as below:

Mainly focus on the “invoice passbook” feature for browsing and importing e-invoices, supplemented by the “invoice carrier setting” feature for accessing the cloud databases.

Only accept the most commonly used carrier type “mobile phone barcode” and do not support advanced features such as “add a new carrier to mobile phone barcode” and ”connect bank account for lottery prize remittance.”

To incentivize users to share their spending records, each e-invoice, whether it is printed out or paperless in the cloud, can be redeemed as cash back of $1 NTD.

Paper e-invoices will be redeemed upon successful scan and import, but e-invoices imported from the cloud database will not, encouraging users to open and interact with the app.

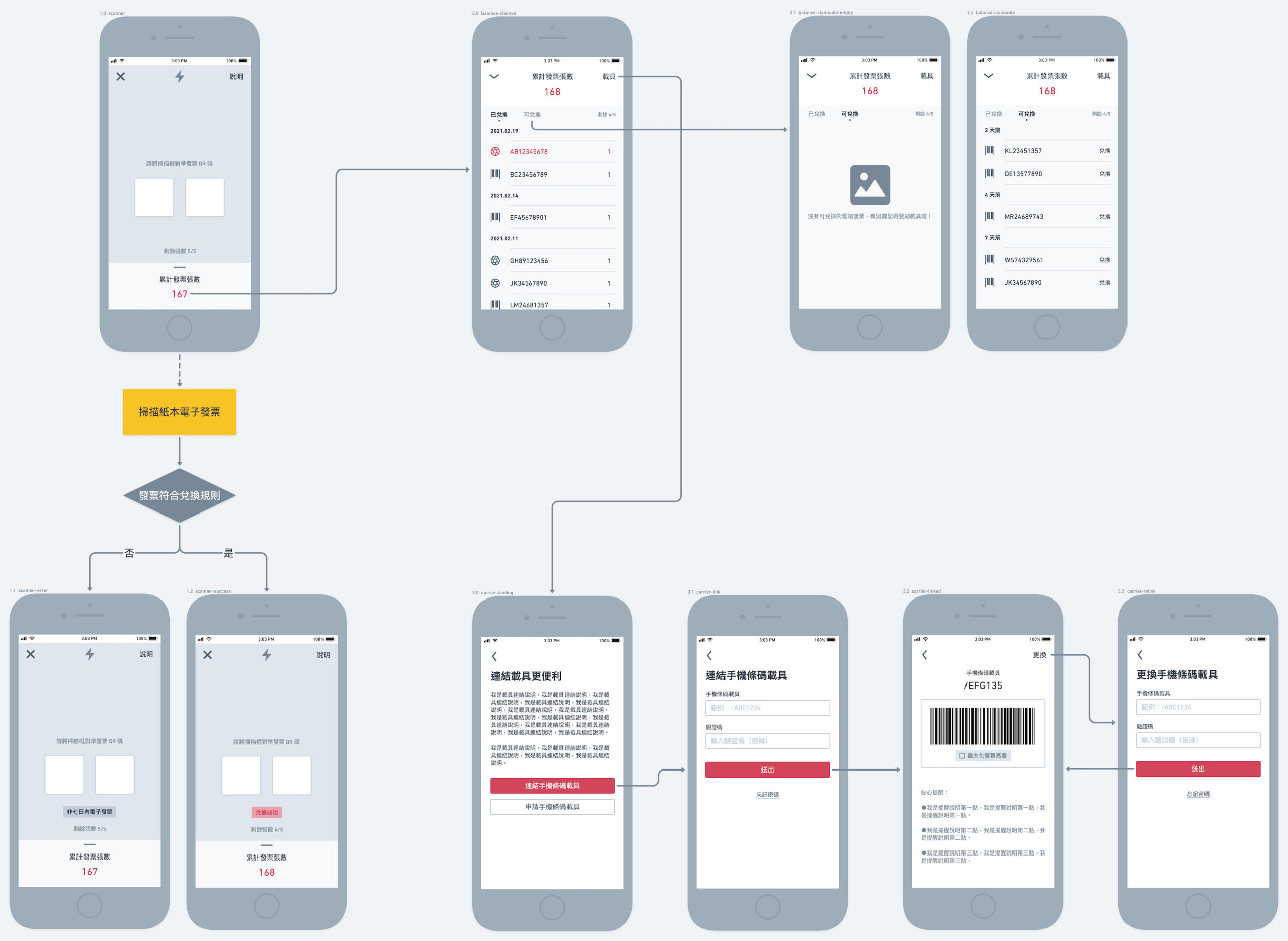

Design

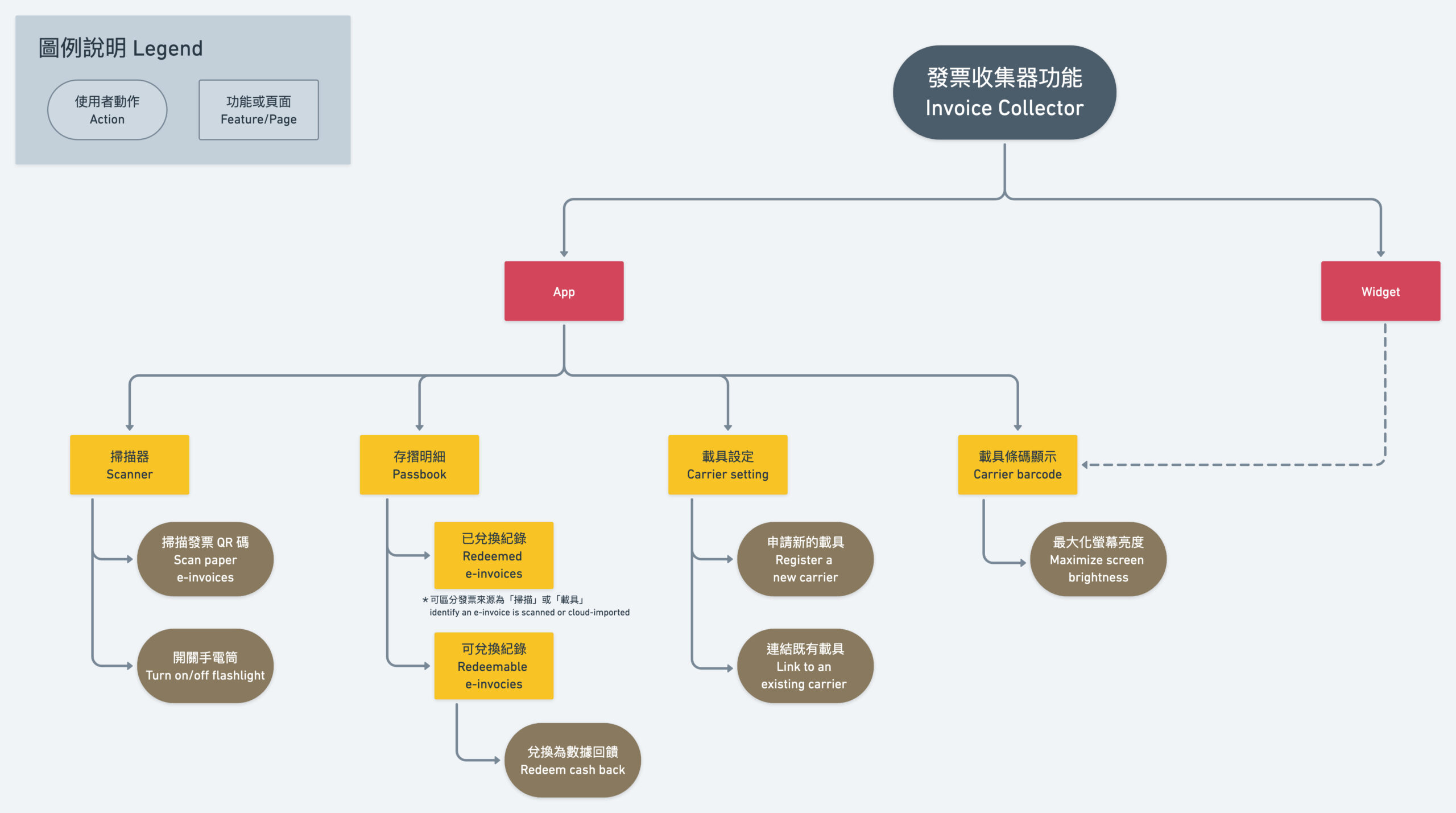

Before I dug into feature planning, I figured out the overall information architecture so that users can easily find their way in the app, followed by detailed specifications, user flow, and wireframes. These materials helped facilitate discussions with the design and engineering team and align everyone’s expectations.

Information architecture

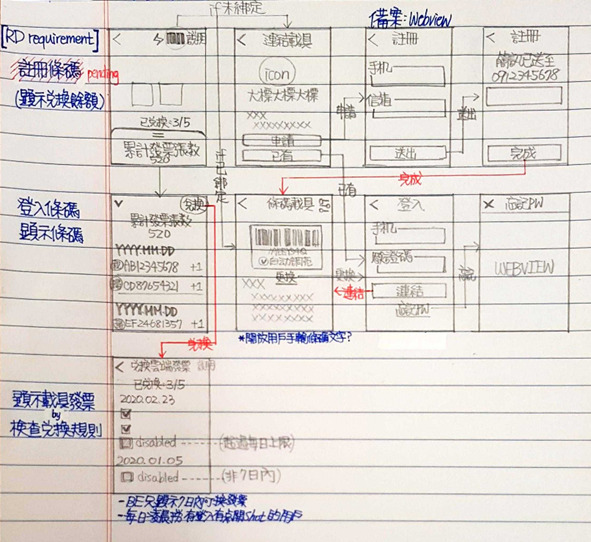

Paper sketch

Wireframe

I’ve created a PRD that demonstrates how I conduct research, define problems and goals, and develop a new product or feature:

Note: currently only available in Traditional Chinese.

Learning & Takeaway

This was my first job and first product management experience! By working in a fast-changing startup company and building this feature from ideation to execution, I learned a few things in the process:

Build product fast yet organized. Product development in a startup environment is fast, and so is the speed of change. That does not mean we need to be disorganized, however. Once changes occur, we should inform all stakeholders in the right way, through the right channel, as soon as possible to ensure that we share the same goals. Never be afraid of over-communication.

Speak the same language with your team members. I could not explain product requirements to the engineering team from their perspective, so the development results differed from expectations several times at first. After teaching myself programming, I learned how to speak in an engineer-friendly way, which shortened discussion time in development meetings and prevented unintended output from happening again.

What is Uniform Invoice?

What is Uniform Invoice?